EchoStar Corporation

Executive Summary:

EchoStar CEO Hamid Akhavan today presented the company's strategic transformation at World Space Business Week, explicitly outlining the pivot from "Asset-Rich, Capital Constrained Operator to Asset-Light Growth Investment." The presentation confirmed all transaction details and timeline, with management expressing confidence in Q1 2026 closing. Charlie Ergen, Chairman, emphasized that this represents "45 years of asset accumulation now being monetized at the perfect moment."

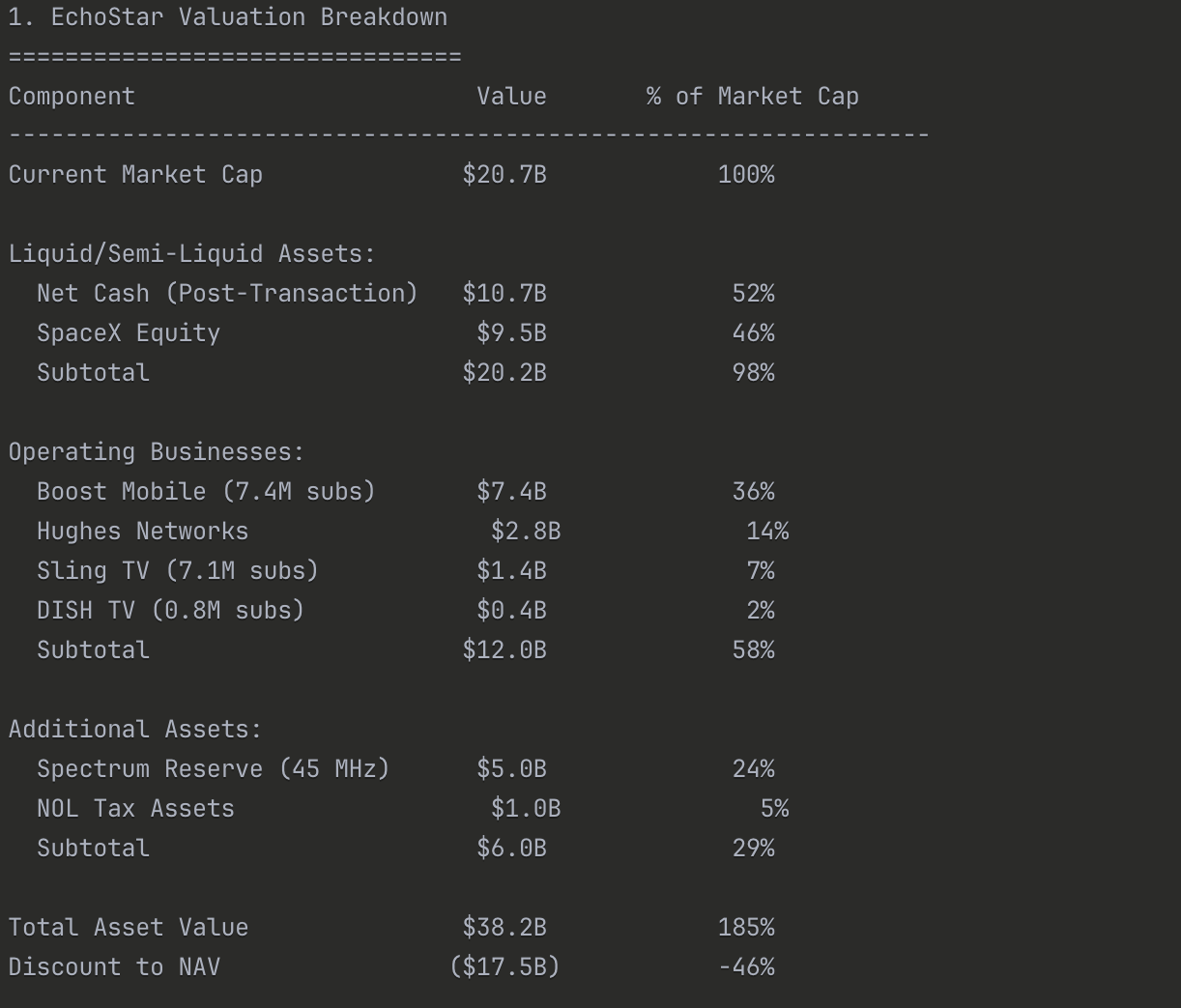

EchoStar Corporation (NASDAQ: SATS) trades at a $20.7B market capitalization while holding $10.7B in net cash and $8.5B in SpaceX equity, & NOL carryover assets exceeding 1b+, before even considering its $15.5B revenue operating business (Sling, Dish, HughesNet) & remaining spectrum assets. The company just announced transformative spectrum sales totaling $40B to AT&T and SpaceX, fundamentally altering its financial profile from distressed net debt to net cash king. Yet inexplicably, the stock trades at a current 20.7b market cap.

Current Stock Price: $70.84 (September 15, 2025)

Market Capitalization: $20.7B

Net Asset Value: $54.2B

Discount to NAV: 62%

Our Price Target: $138

I. The Transformation Story: From Distress to Fortress Balance Sheet

The Dire Starting Point (Early 2025)

EchoStar entered 2025 as a company on the brink. Crushed under $26.9B in total debt with a CCC+ credit rating signaling distress, the company was burning through $2B in cash annually while facing an FCC investigation into its spectrum warehousing practices. The market had essentially written off the equity, with bankruptcy concerns dominating any discussion of the company's future. Legacy satellite TV businesses were hemorrhaging subscribers, the ambitious 5G network buildout was devouring capital, and Charlie Ergen's complex financial engineering had exhausted investor patience after two decades of promises.

The Catalyst: Regulatory Pressure Becomes Salvation

The FCC's investigation, initially viewed as another negative catalyst, paradoxically forced the value-unlocking transactions the market had been waiting for. Under pressure to deploy or divest spectrum assets, EchoStar negotiated two landmark deals that will inject over $40B in value while solving both its debt crisis and strategic positioning challenges in one master stroke.

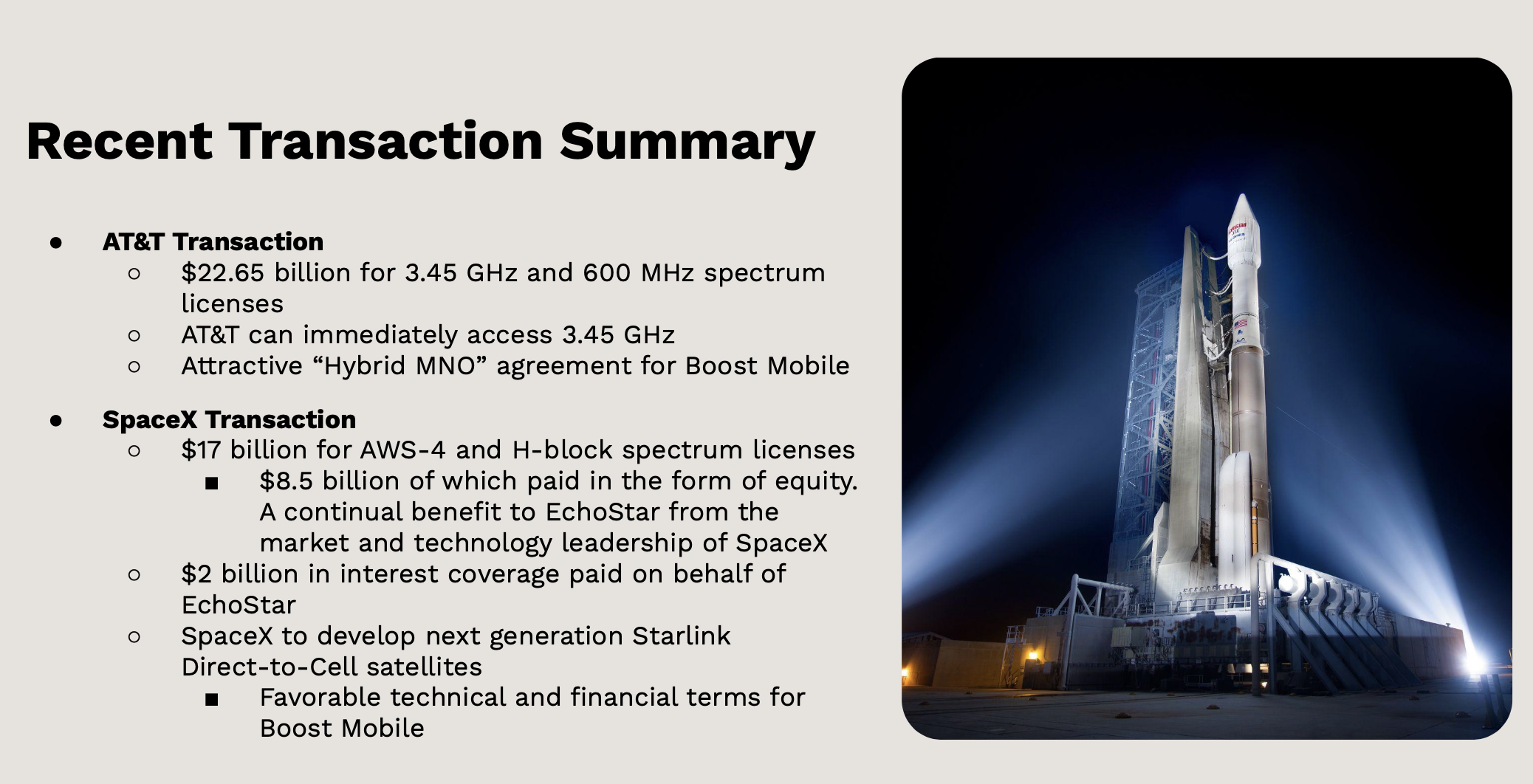

The AT&T Transaction: $22.65B in Pure Cash

AT&T Transaction: Announced Aug 2025 for $23B (30 MHz 3.45 GHz + 20 MHz 600 MHz spectrum); pending FCC approval, expected close mid-2026; AT&T to deploy for 5G expansion.

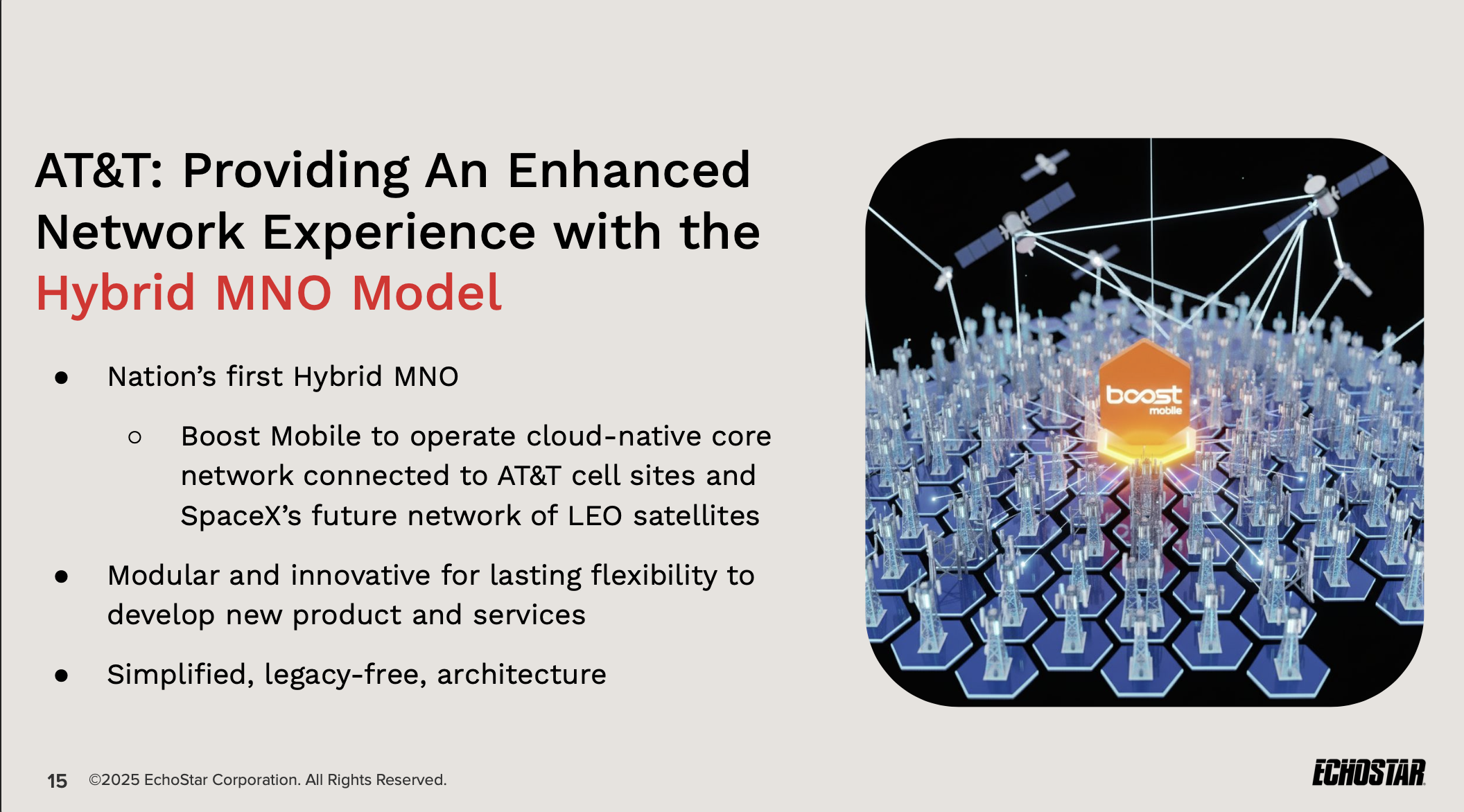

AT&T agreed to purchase EchoStar's 3.45 GHz and 600 MHz spectrum licenses for $22.65B in an all-cash transaction. This isn't merely a financial transaction - it includes a transformative "Hybrid Mobile Network Operator" agreement that fundamentally repositions Boost Mobile in the wireless landscape. Under this arrangement, Boost gains immediate access to AT&T's entire nationwide tower infrastructure, instantly transforming from a struggling MVNO into a facilities-based carrier with genuine network control. The deal provides AT&T with crucial mid-band spectrum for 5G densification while giving Boost the foundation for nationwide coverage without the capital burden of tower construction.

The SpaceX Partnership: $17B Plus Revolutionary Technology Access

*SpaceX Transaction: Announced Sep 8, 2025 for $17B ($8.5B cash + $8.5B stock; AWS-4/H-block spectrum); pending FCC approval, expected close mid-2026; SpaceX to accelerate Starlink direct-to-cell launch.

The SpaceX transaction represents far more than a simple spectrum sale. For $17B in total consideration, SpaceX acquires the AWS-4 and H-Block spectrum licenses critical for its Starlink direct-to-cell satellite service. The structure - $8.5B in cash plus $8.5B in SpaceX equity - creates an ongoing partnership that positions both companies at the forefront of hybrid terrestrial-satellite communications.

Critically, SpaceX also assumes $2B of EchoStar's debt service obligations through 2026, providing immediate cash flow relief. The strategic elements extend beyond the financial: Boost Mobile becomes Starlink's exclusive terrestrial MNO partner, gaining access to revolutionary satellite-to-phone technology that will enable true 100% geographic coverage across North America. No dead zones in rural areas, no coverage gaps in remote locations - a unique selling proposition no other carrier can match.

The SpaceX equity component, initially valued at $8.5B when the deal was struck at a $400B SpaceX valuation, has already appreciated to $9.5B as SpaceX's valuation climbed to $449.29B in the private secondary market. This 12% gain in mere months demonstrates the quality of the asset EchoStar is receiving.

II. The Pro Forma Financial Architecture

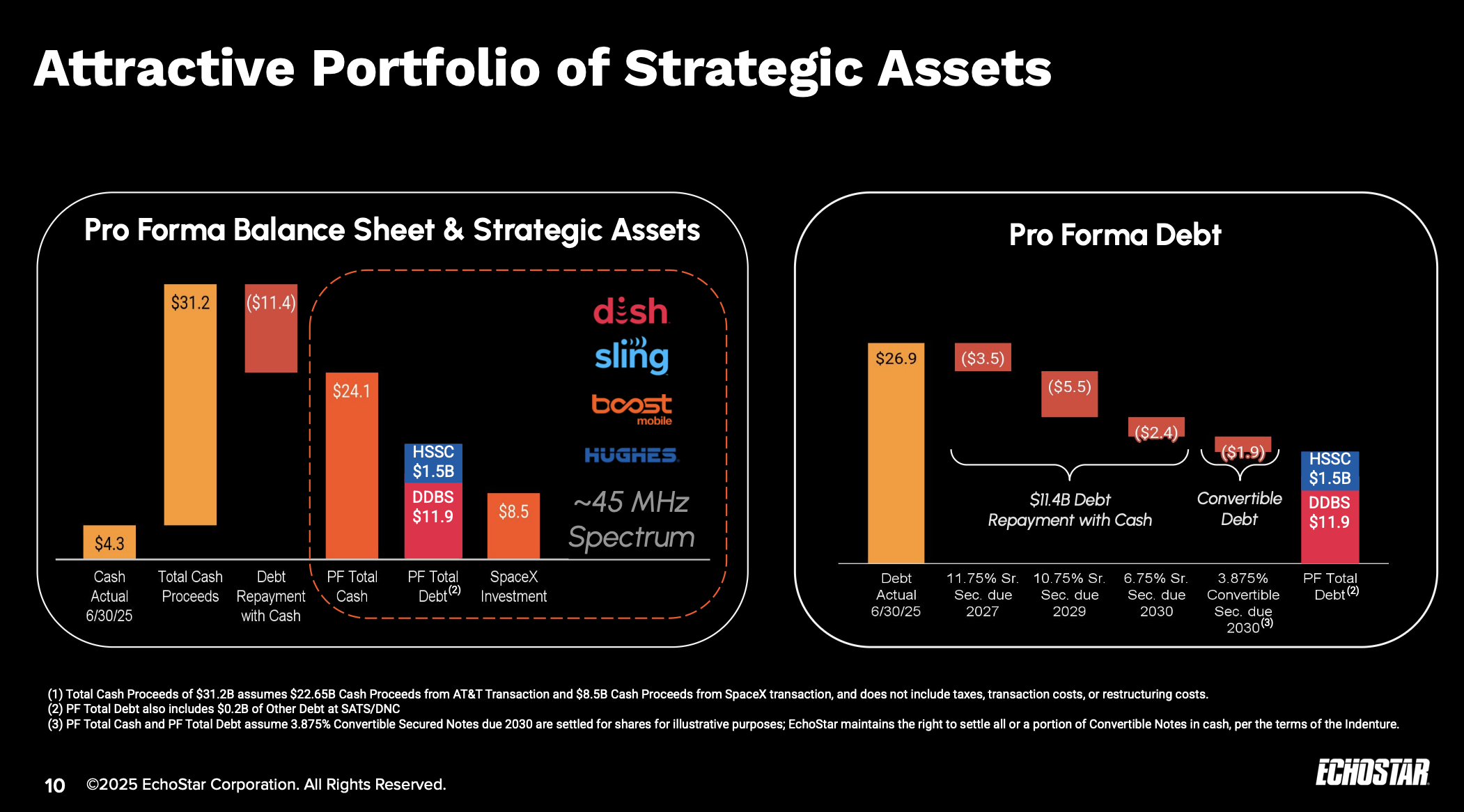

Balance Sheet Transformation

The numerical transformation defies belief for a company that seemed headed toward restructuring:

Not including tax on net proceeds ~ likely meaningfully offset by NOL.

Pre-Transaction Balance Sheet:

- Total Debt: $26.9B

- Cash: $4.3B

- Net Debt: $22.6B

- Annual Interest Expense: $1.75B

- Credit Rating: CCC+ (deep junk territory)

Pro Forma Balance Sheet (Post-Closing Q1 2026):

- Gross Cash: $24.1B

- Remaining Debt: $13.4B (primarily convertible notes)

- Net Cash: $10.7B

- SpaceX Equity: $9.5B (liquid in secondary markets)

- NOL Tax Assets: $1.0B+ (Federal, State, Foreign carryforwards)

- Annual Interest: Minimal (SpaceX covering $2B through 2026)

- Credit Trajectory: Clear path to investment grade

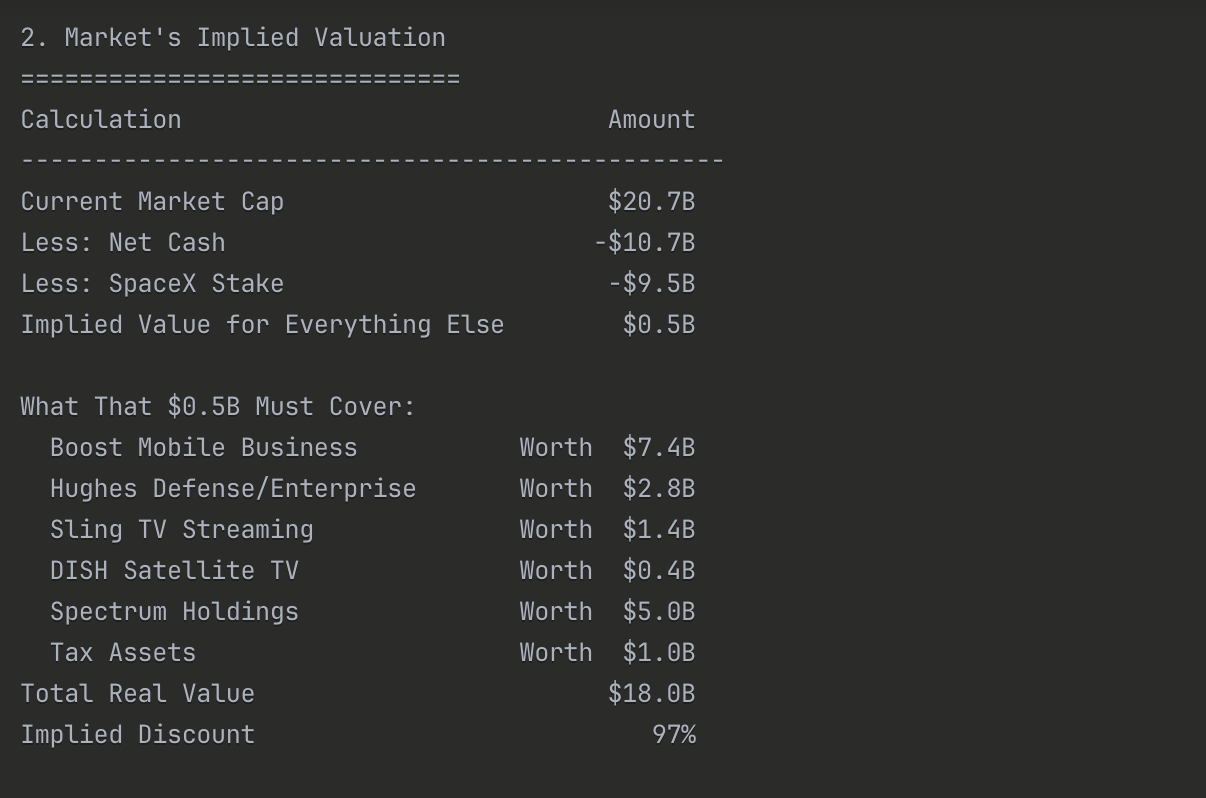

The Financial Position Summary:The swing from $22.6B net debt today to $10.7B net cash post-closing represents a $33.3B improvement in net financial position.

Total Liquid/Semi-Liquid Assets Post-Transaction:

- Net Cash: $10.7B

- SpaceX Stake: $9.5B

- NOL Tax Shield: $1.0B

- Total: $21.2B in value vs. $20.7B current market cap

This means the market is valuing the entire operating business ($15.5B revenue, 15.3M subscribers) and remaining spectrum (~45 MHz) at negative $500M - an impossibility that highlights the magnitude of the mispricing.

Model SpaceX's continued growth? EchoStar, is certainly mispriced and materially at an inflection point in a bullish direction.

Ergen mentioned today as well that EchoStar has no plans to sell their stake in SpaceX in the foreseeable future — opening the arbitrage for NAV rebalancing against secondary spot price for SpaceX against EchoStar market cap.

Free Cash Flow Renaissance

The operational transformation is equally dramatic. Currently, EchoStar burns approximately $2B in annual free cash flow, crushed by massive capital expenditure requirements for 5G network buildout and punishing debt service interest expenses. Post-transaction, the picture transforms entirely:

Current Cash Flow Profile:

- EBITDA: $3.1B (20% margin on $15.5B revenue)

- Growth CapEx: ($2.0B) for 5G buildout

- Interest Expense: ($1.75B)

- Free Cash Flow: ($2.0B)

Current Cash Flow Profile (Burning Cash):

- EBITDA: $3.1B

- Growth CapEx: ($2.0B) - 5G network + LEO satellite buildout

- Interest Expense: ($1.75B) on $26.9B debt

- Other/Working Capital: ($350M)

- Current FCF: Negative ($2.0B) - burning cash

Pro Forma Cash Flow Profile (After Deals Close ~ AT&T + SpaceX):

- EBITDA: $3.1B (maintained at 20% margin)

- Maintenance CapEx: ($400M) - 5G build complete, LEO canceled

- Interest Expense Through 2026: $0 (SpaceX covers $2B debt service)

- Interest Expense Post-2026: ~($500M) on $13.4B remaining debt

- Operating Efficiencies: $400M from simplification

- Pro Forma FCF (Through 2026): $2.6B annually

- Pro Forma FCF (Post-2026): $2.1B annually

The Cash Flow Swing:

- Current: Negative $2.0B (burning cash)

- Pro Forma: Positive $2.6B (generating cash)

- Total Improvement: $4.6B annual swing

The key drivers: Eliminating $1.6B in growth capex, eliminating $1.75B in interest (SpaceX covers through 2026), and operational improvements. This takes them from cash-burning distress to cash-generating stability.

The $4.6B annual swing from burning $2B to generating $2.6B in free cash flow at the current market cap implies a forward P/FCF multiple of just 8x - absurdly cheap for a company with EchoStar's remaining strategic assets and balance sheet.

III. The Remaining Business Post LME ~ (What the market currently isn't valuing correctly)

Boost Mobile: America's First Hybrid MNO (7.4M Subscribers)

Boost Mobile emerges from these transactions as something entirely new in American wireless - a true hybrid Mobile Network Operator combining terrestrial and satellite coverage. With access to AT&T's nationwide tower network and exclusive partnership rights to Starlink's direct-to-cell technology, Boost can offer arguably the best coverage of all MNOs with genuine 100% geographic coverage.

The 7.4M subscriber base, while modest compared to the majors, represents a valuable foundation for growth. At industry-standard valuations of $1,000-1,500 per subscriber, Boost alone justifies $7.4-11B in value. The unique coverage proposition positions it to capture rural and enterprise customers who need guaranteed connectivity everywhere.

Hughes Network Systems: The Crown Jewel Hidden in Plain Sight (MILSATCOM)

Hughes represents one of the most under-appreciated assets in the portfolio, with a $1.8B contracted backlog spanning defense, aviation, and enterprise customers. The business operates across multiple satellite orbits (GEO, MEO, LEO), positioning it perfectly for the hybrid future of satellite communications. Major airlines depend on Hughes for in-flight connectivity, while defense and intelligence agencies rely on its secure communications networks with multi-orbit SATCOM and software-defined networking capabilities.

The transformation with debt removed: Previously unable to bid on major IDIQ (Indefinite Delivery/Indefinite Quantity) contracts due to CCC+ credit rating and bonding requirements, Hughes can now compete for multi-billion dollar DoD programs just as Pentagon spending on resilient space communications accelerates. The SpaceX partnership opens new doors - Hughes's ground systems expertise perfectly complements SpaceX's Starshield military satellites, creating a unique combined offering. With investment grade credit approaching, Hughes can finally invest in growth rather than managing attrition decline in consumer cyclical, pursue strategic accretive M&A, and expand R&D with FCF improvements post LME. The company's "best-in-class" ESA (Electronically Steerable Antenna) technology for mobile military platforms positions it at the center of DoD's shift to distributed, software-defined architectures.

The opportunity: EchoStar can finally fund Hughes's growth ambitions rather than starve it of capital. This $1.8B backlog business could double as it captures share in the $100B+ DoD space modernization budget - but the market values it at essentially zero, still seeing "dying satellite company" rather than emerging defense prime.

Sling TV: The Streaming Success Story (7.1M Subscribers)

While the market obsesses over DISH's dying satellite TV business, it completely overlooks Sling TV's successful pivot to streaming. With 7.1M subscribers growing at 18% year-over-year and recently ranked as the "Best Live Streaming Service" by US News & World Report, Sling represents the successful transformation from linear to streaming that many legacy media companies have failed to achieve.

At typical streaming multiples of $200-300 per subscriber, Sling represents $1.4-2.1B in value. The lean cost structure and targeted content offering position it well in the fragmented streaming landscape.

DISH TV: Nothing Exciting

DISH TV - 0.8M subs generating $1.1B revenue, worth $400M+ even at distressed multiples

The Spectrum Reserve: $5B

Even after the massive sales to AT&T and SpaceX, EchoStar retains approximately 45 MHz of valuable nationwide spectrum. At current market rates of $0.20-0.40 per MHz-POP, this represents $4-6B in additional value that could be monetized opportunistically or deployed for strategic purposes.

Tax Assets: The $1B Shield

EchoStar carries $1.02B in Net Operating Loss carryforwards ($543M federal, $277M state, $201M foreign) that will shield future income from taxation. These NOLs mean the company can generate substantial pre-tax income without cash tax obligations, maximizing cash retention during the transformation period.

IV. Why the Market Is Completely Wrong

The Technical Selling Tsunami

The stock's weakness despite transformative news stems from massive technical selling pressure with virtually no natural buyers. The DISH-EchoStar merger created enormous RSU (restricted stock unit) vesting events, with employees receiving shares now dumping them regardless of price. Merger arbitrage funds that played the DISH-EchoStar spread are mechanically unwinding positions. Quarter-end window dressing means institutional investors don't want to show this controversial name on their 13F filings.

This technical pressure meets a complete absence of natural buyers.

We did although get $100+ price targets from Deutsche bank ($102) + TD Cowen ($100).

The Charlie Ergen Discount

After two decades of complex financial engineering, the market has developed an almost pathological distrust of Charlie Ergen. Previous spectrum transactions that sounded transformative somehow never translated to shareholder value. The 5G network buildout consumed billions with little to show. Minority shareholders have repeatedly watched promising developments fail to materialize into returns.

This "Charlie discount" - estimated at 30-40% by several analysts - means the market simply doesn't believe the transformation story until cash literally hits the balance sheet. The irony: this time the deals are materially real, the cash is coming, and the government itself is pushing for completion ~ (FCC / Trump)

The Complexity Problem

Modern markets struggle with complexity, and EchoStar presents a masterclass in confusion. Is it a satellite company? A wireless carrier? A spectrum holding company? Defense company? The answer - all of the above - doesn't fit neatly into quantitative models or sector classifications. The pro forma analysis requires understanding spectrum values, satellite technology, wireless economics, and streaming dynamics. Honestly, it is very confusing — we have even had to update our model & valuation 5 times in September — with help of the X community.

V. The Catalysts That Will Force Re-Rating

Q4 2025: Regulatory Approvals

The FCC, having pushed for spectrum deployment, needs these transactions to succeed to validate its regulatory approach. Both AT&T and SpaceX have massive incentives to close quickly. The government wants American 5G leadership and rural broadband coverage - both transactions advance these goals.

Q1 2026: Cash Arrives, Debt Disappears

When $24.1B in cash hits the balance sheet and debt plummets from $27B to $13B, the transformation becomes undeniable. Financial screens will show EchoStar as net cash positive. Credit rating agencies will begin upgrade cycles.

2026-2027: Operations Prove Out

As Boost Mobile launches true nationwide coverage via Starlink integration ~ as hinted today, subscriber trends should inflect positively — In fact, I am going to switch providers from AT&T. Hughes's multi-orbit capabilities position it for the LEO constellation boom. Sling continues getting its fair share in streaming. The operational narrative shifts from decline to growth.

2027+: SpaceX Liquidity Event

SpaceX's inevitable IPO or secondary transactions will crystallize the value of EchoStar's stake. ARK Invest projects SpaceX could reach $2.5 trillion by 2030. Even at a fraction of that optimism, EchoStar's stake could be worth $20-30B vs todays est. 20.49b valuation.

VI. Valuation: Multiple Methods, Same Conclusion

Liquidation Analysis (Disaster Scenario)

Even if everything fails and the company liquidates:

- Net Cash: $10.7B

- SpaceX (secondary market liquidity): $9.5B

- Boost (7.4M × $300 distressed): $2.2B

- Hughes/Sling (50% of book): $1.5B

- Spectrum (fire sale): $2.0B

- Satellites/Infrastructure: $1.0B

- Total: $26.9B vs $20.7B market cap (30% upside to liquidation)

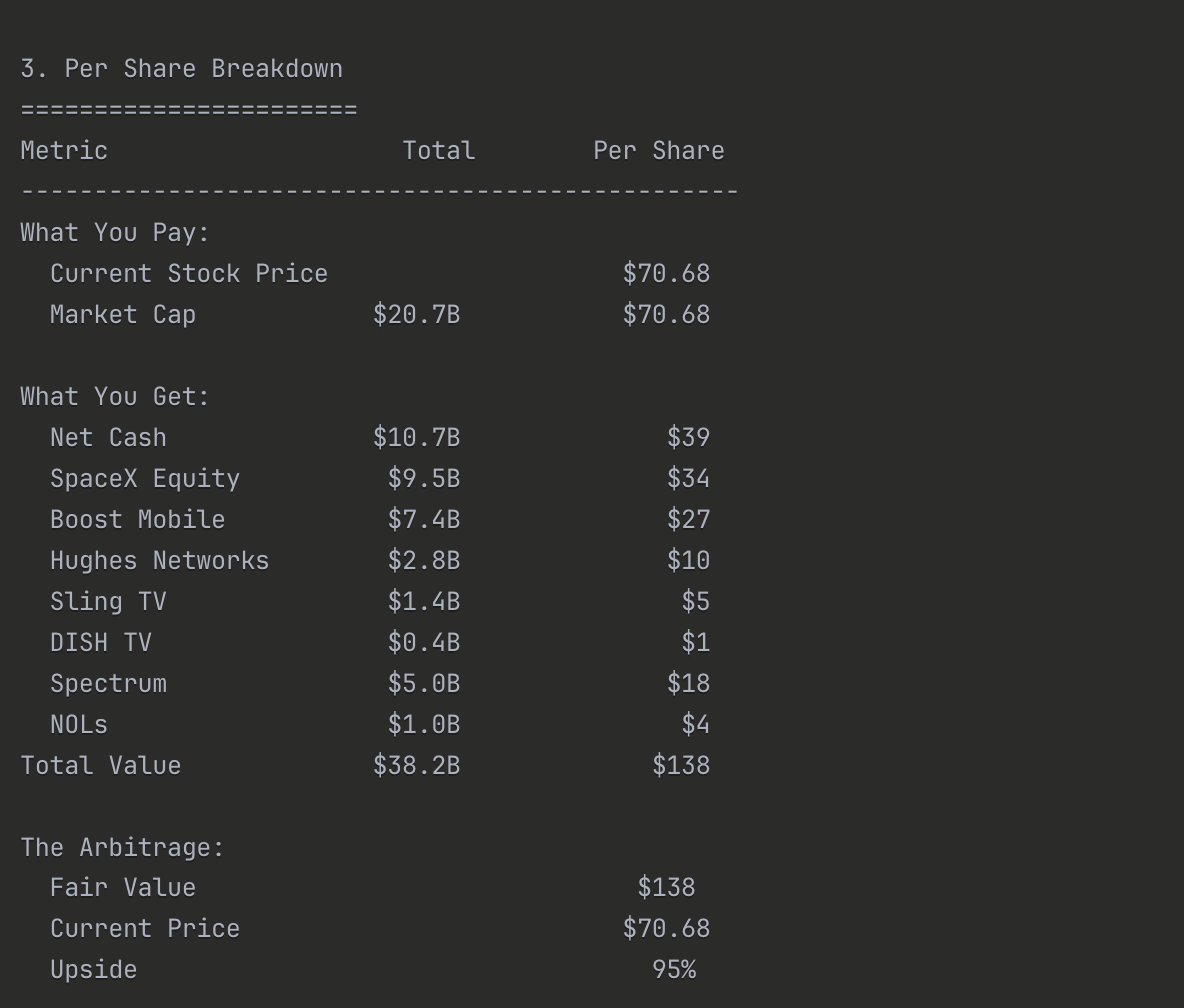

Sum-of-Parts (Current Marks)

- Net Cash: $10.7B

- SpaceX Equity: $9.5B (at $449B valuation)

- Boost Mobile: $7.4B (1000/sub)

- Hughes: $2.8B (1.5x revenue)

- Sling TV: $1.4B ($200/sub)

- DISH TV: $0.4B ($500/sub)

- Spectrum: $5.0B ($0.30/MHz-POP)

- NOLs: $1.0B

- Less: Debt: ($13.4B)

- Total NAV: $54.2B ($195/share vs $70.68 current)

DCF Valuation (10x Terminal Multiple)

- 5-Year PV of $2.6B FCF: $10.4B

- Terminal Value: $26B

- PV of Terminal: $17.7B

- Plus: Net Cash: $10.7B

- Plus: SpaceX: $9.5B

- Plus: Remaining Spectrum: $5.0B

- Total: $52.9B ($191/share)

Every methodology points to massive undervaluation.

VII. The Risk/Reward Is Completely Skewed

Downside Protection

At $70.68, you're protected by:

- Liquidation value 30% higher

- Net cash + SpaceX = 97% of market cap

- Fortune 250 company with $15.5B revenue

- Government ensuring deal completion

Upside Potential

- Base Case (1x NAV): $195/share (176% upside)

- Reasonable Case (market recognition): $150/share (112% upside)

- Bull Case (SpaceX $600b + ops improve): $250/share (254% upside)

- Dream Case (SpaceX IPO $1T+): $350/share (395% upside)

VIII. Conclusion: The Market Has Lost Its Mind

At $70.68, EchoStar trades at the same price essentially before the announcement with SpaceX, despite announcing now in total over $40B in transformative transactions that create a net cash position and strategic partnerships with AT&T and SpaceX. The market is literally valuing the company as if nothing has changed.

This isn't a complex thesis requiring brilliant insights. It's simple arithmetic: you're buying $54B in assets for $21B. The net cash and SpaceX stake alone nearly cover the entire market cap. Everything else - a $15.5B revenue business, 15.3M subscribers, valuable spectrum, strategic partnerships - comes free.

This is the opportunity: buying a Fortune 250 company below liquidation value while transformative catalysts approach.

Important Disclosures & Disclaimers ¹

Informational Purposes Only – This research report is provided exclusively for educational and informational purposes. It does not constitute investment advice or a recommendation to buy, sell, or hold any security and should not be relied upon as such.

Forward‑Looking Statements – Certain statements herein contain forward‑looking projections, estimates, or other “forward‑looking statements” (as defined under the U.S. Private Securities Litigation Reform Act of 1995). Such statements are inherently uncertain; actual results may differ materially from the views expressed. The author undertakes no obligation to update any forward‑looking statement.

Accuracy & Completeness – The information contained in this report is believed to be accurate at the time of publication; however, no representation or warranty, express or implied, is made regarding its accuracy, completeness, or timeliness. All data should be independently verified.

Risk of Loss – Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Readers should perform their own due diligence or consult a registered investment professional before making any investment decision.

Author’s Position – As of the publication date, the author beneficially owns a long position in EchoStar (NASDAQ: SATS) representing 5,375 shares. The author may alter this position at any time without further notice. No specific share count or cost basis is disclosed.

No Offer or Solicitation – Nothing herein shall be construed as an offer to sell, or the solicitation of an offer to buy, any security.

Research & AI-Assistance Disclaimer

This report was prepared with the assistance of Claude Opus 4.1 large-language model. All quantitative data, charts, and tables were derived from publicly available sources—including SEC filings (10-K, 10-Q), earnings releases, and third-party financial databases—each of which is hyper-linked in the body of the article for verification.

While every effort was made to ensure numerical accuracy and interpretive fairness, the analysis reflects the author’s opinions at the time of writing and may contain inadvertent errors or omissions. Nothing herein constitutes investment advice, a recommendation, or a solicitation to buy or sell any security. Investors should conduct their own due diligence and consult a qualified financial professional before making investment decisions.

.png)

.png)

.png)